Best USD Business Solutions for Cross-Border Banking in 2026

For many Canadian businesses, cross-border banking is now part of everyday operations. From paying for US-based software and contractors to collecting revenue from American customers, USD transactions are now a standard cost of doing business.

The challenge is that many companies still handle these transactions through systems that were never designed for frequent, high-volume USD activity. Traditional bank USD accounts, CAD cards used for USD purchases and disconnected FX tools often introduce unnecessary fees, delays and operational blind spots.

Let’s talk about those fees for a minute. Rising operating costs are one of the top three financial concerns for small businesses in Canada, and most owners watch margins carefully. Every dollar lost on fees could be spent elsewhere.

This guide breaks down what Canadian businesses need to know about modern USD banking in 2026. We will look at why USD access matters, what features actually make a difference, how to evaluate your options and how to set up a USD workflow that supports growth rather than draining profit margins.

Why Canadian businesses need USD banking solutions

Canadian and US economies are intertwined in many ways, and even businesses that operate entirely from Canada often rely on US vendors, platforms or customers. The result is that most companies will touch USD in some way, whether they plan to or not.

More cross-border activity than many businesses realize

Many small businesses assume a USD business account in Canada is only necessary once they have US customers or employees. In practice, USD exposure shows up much earlier. Software subscriptions, cloud services, advertising platforms, logistics providers and professional services frequently charge in USD. Over time, these costs add up.

For businesses earning revenue in USD, the stakes are even higher. Accepting payments in USD and converting them inefficiently can erode margins, especially when FX fees are opaque or inconsistent.

The importance of invoicing and collecting in USD

Invoicing US customers in USD is table stakes these days; a baseline expectation for doing business across the border. It reduces friction for buyers and can expedite payments. Without a proper USD setup, however, Canadian businesses may face delays, extra fees or forced currency conversions when receiving funds.

A USD business account that Canadian businesses can rely on allows companies to receive USD via ACH or wire and hold those funds. They can decide when and how to convert them rather than being forced into automatic conversions at unfavourable rates.

Reducing foreign exchange costs

FX costs are one of the most underestimated expenses in cross-border banking. Many businesses focus on advertised rates while missing the full picture. Traditional banks often apply FX markups that are difficult to see, sometimes charging businesses multiple times across account fees, transaction fees and conversion spreads.

Over time, these costs compound. What feels like a small percentage on each transaction can add up to thousands of dollars annually. By using Float, businesses can convert funds to and from USD with rates that are 90% less than traditional banks.

Operational and cash flow benefits

A dedicated USD financial workflow also delivers operational advantages that go beyond cost savings. They give finance teams clearer insight into cash flow.

A few benefits to note:

- Faster payments when transacting in USD, especially through ACH rather than international wires

- Cleaner accounting and reconciliation by keeping USD inflows and outflows separate from CAD activity

- Better working capital management by holding USD balances when appropriate instead of converting immediately

Key features to look for in a USD business banking solution

Not all USD solutions are created equal. Some features sound appealing on paper but offer limited real-world value. Others become critical as transaction volume increases.

Essential account capabilities

At a baseline, a USD solution should allow you to hold, send and receive USD without unnecessary friction. Look for an account that supports ACH payments, incoming USD transfers and easy access to balances without manual workarounds.

Transparency is key with foreign currency accounts. FX rates should be clearly stated, consistent and easy to understand, regardless of transaction size.

Payments and spending

USD payments for Canadian businesses fall into a few common categories:

- ACH payments from US customers

- USD bill payments to vendors and suppliers

- USD corporate or virtual cards for recurring expenses

- Wire transfers for larger or international payments

A modern solution should support all of these without forcing businesses to juggle multiple tools.

USD spending tools are particularly important for day-to-day operations. Using CAD cards for USD purchases often triggers foreign transaction fees of 2.5% or more. NOTE: Foreign transaction fees happen at the moment of purchase and are almost always higher than foreign exchange or conversion fees, like Float’s 0.25%, which happen in an account. Over time, making USD purchases this way will mean your total fees really add up—potentially as much as 10x versus relying on direct conversion.

Digital tools and integrations

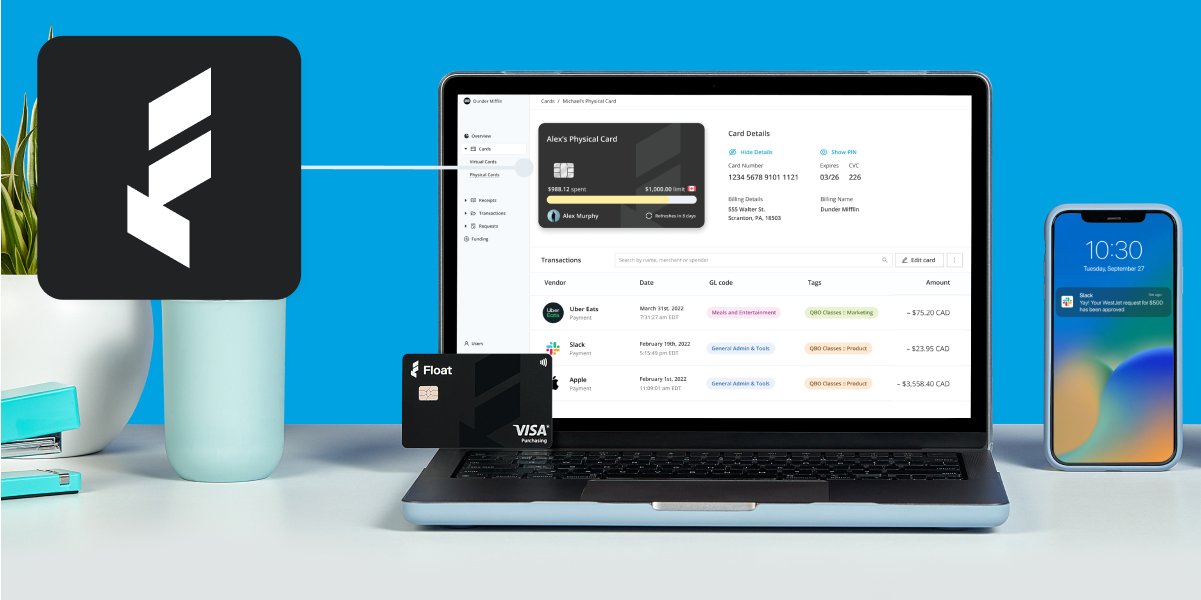

USD banking shouldn’t live in a silo. Instead, an online-first experience with real-time visibility allows teams to track balances, payments and conversions as they happen.

Strong accounting integrations with platforms like QuickBooks, Xero or NetSuite help ensure USD activity flows cleanly into financial reporting. This reduces manual reconciliation and speeds up month-end close.

Types of USD business banking solutions available to Canadian companies

Canadian businesses generally encounter three broad categories of USD solutions. The right choice depends less on brand names and more on how well each option handles fees, visibility and the realities of ongoing cross-border activity.

Digital-first USD banking platforms

Fintech platforms designed for cross-border businesses aim to simplify USD operations by combining accounts, FX and payments in one place. These platforms often offer competitive FX rates, faster setup and modern tooling.

The biggest advantage is consolidation. When USD banking, FX and spending live in a single platform, businesses gain a better line of sight into spending and reduce the risk of errors caused by fragmented systems.

What’s important to note is that while many of these digital-first USD banking platforms were designed primarily for US businesses and later adapted for Canada, Float was purpose-built for companies here at home. Beyond just looking for modern providers, Canadian businesses should evaluate whether a provider properly supports Canadian tax workflows, CAD and USD operations, and local payment rails like EFT and ACH.

Traditional bank with USD accounts

Most Canadian banks offer USD accounts as an add-on to existing business banking relationships. While familiar, these accounts often come with monthly fees, per-transaction charges and black-box FX pricing.

Banks may also impose limits on ACH transactions or charge extra for incoming and outgoing USD payments. For small businesses, negotiating better rates can be difficult without significant volume.

Multi-currency business accounts

Some providers offer foreign currency accounts that support multiple currencies, including USD. These can be useful for businesses operating in several markets.

However, businesses should look closely at how FX is handled, how spending works and whether the platform integrates with their existing accounting tools. A multi-currency account that operates as a point solution can still introduce complexity.

How to choose the right USD banking solution

Selecting the right USD financial operations setup requires looking beyond surface-level pricing and feature lists. Moving money is relatively easy. Doing it efficiently, without creating extra work for your team, is where the real difference shows up. What works well at 10 transactions a month can feel very different at 100.

1. Assess your business needs

Start by understanding how your business uses USD today and how that might change. This context helps determine whether you need basic access or a more robust solution.

Consider these variables:

- Whether you primarily pay in USD, receive USD or both

- How frequently you transact in USD

- Whether USD spending is recurring or project-based

2. Compare costs beyond the headline

Headline FX rates tell only part of the story. Many businesses underestimate costs because they’re buried in statements rather than itemized clearly.

It’s wise to keep the details in mind:

- Monthly account fees

- Per-transaction charges for ACH or wires

- Foreign transaction fees on cards

- FX spreads applied during conversions

3. Evaluate platform fit

Ease of use matters. A solution that requires multiple dashboards, exports or manual steps can create more work than it saves. Look for platforms that integrate USD activity with your broader financial operations, including accounting, approvals and reporting.

Setting up USD business banking as a Canadian company

Getting started with USD banking is typically straightforward, but requirements vary by provider. The difference is often less about complexity and more about how much friction you are willing to tolerate along the way.

What you will need to set up a USD bank account

Having a few basic documents ready can speed up setup. You can expect that most providers will require:

- Canadian incorporation documents

- Business identification and address

- Verification of authorized signers

- Potential US tax information, depending on how funds are received or held

What the setup process looks like

Modern platforms often allow businesses to open USD accounts in minutes rather than weeks. Traditional banks may require additional paperwork or in-branch visits.

Once the account is live, businesses can connect payment methods, issue USD cards and begin transacting.

Implementation tips

Plan the transition carefully. Update vendor payment details, notify customers of new payment options and ensure accounting systems are configured correctly.

Even though switching providers takes effort, many businesses find that the long-term savings and clarity are worth it.

Maximizing value from your USD banking setup

A USD account is only as effective as how you use it. Opening the account is the easy part, but getting real value from it takes a bit more thought.

Strategic currency management

Deciding when to convert versus hold USD depends on cash flow needs and exposure. Businesses that convert every USD inflow immediately may miss opportunities to reduce FX costs. Having the flexibility to hold USD and convert on your own timeline can provide meaningful savings.

Smarter payment operations

Efficient payment strategies can reduce costs and improve control. These practices help finance teams maintain visibility without slowing the business down:

- Use ACH instead of wires where possible

- Batch payments to reduce transaction fees

- Automate recurring vendor payments

- Apply approval workflows to manage spend

Leveraging additional features

Many modern platforms offer features that extend beyond basic USD handling, such as high-yield USD balances, virtual cards for online purchases, expense tracking and access to USD credit or working capital options. Used thoughtfully, these tools can support growth while keeping risk in check.

Special considerations by business type

Different business models face different USD challenges. What works for an e-commerce brand can fall apart quickly for a services firm or non-profit, so let’s dig into a few differences.

E-commerce and online businesses

E-commerce companies often deal with high volumes of USD transactions across payments, advertising and logistics. Efficient USD payments for Canadian businesses in this category can have an outsized impact on margins.

Service-based companies

Agencies, consultants and SaaS providers frequently invoice US clients in USD while paying global contractors in other currencies. A clean USD workflow simplifies billing and reconciliation.

Non-profits and organizations

Non-profits receiving USD donations or grants benefit from transparency and low fees. Predictable FX costs help ensure more funds go toward mission-driven work.

Final takeaway for cross-border banking in 2026

Cross-border banking doesn’t have to be a black box. For Canadian businesses, USD exposure is often unavoidable, but unnecessary costs and complexity are not.

When finance flows more smoothly, growth becomes easier to manage. Understanding how USD flows through your business will help you choose a solution built for transparency, while integrating USD activity into your broader financial operations will reduce friction and protect margins.

If your current setup treats USD as an afterthought, 2026 is a good time to revisit it. Modern platforms like Float now make it possible to manage CAD and USD side by side, with clear pricing, real-time visibility and tools designed for how Canadian businesses actually operate.